Introduction

Modernization in banking is no walk in the park, as you well know. It can be incredibly time-consuming and costly — and that’s even with a clear plan and strategy. But in this guide, you’ll get a holistic overview of the key concepts you’ll need to understand while creating your bank’s modernization strategy and planning for the future.

Part 1: digital transformation

What is digital transformation in banking?

Digital transformation in banking is the integration of technologies into the areas that can best benefit from them, fundamentally changing how your bank operates and delivers value to its customers. Don’t think of it as a project, but rather as a total reinvention of your bank’s operating model, its structure, its culture, and its technology. As you can see, digital transformation is about so much more than just tech, and that means it's also a team sport, requiring the involvement of a cross-functional squad, as well as a trusted strategic partner.

Why does my bank need to pursue a digital transformation?

There’s a million reasons why banks are feeling the pressure these days, but let’s narrow it down to just three:

- Rising customer expectations — your customers have become accustomed to the highest level of digital convenience, and many banks aren’t yet able to compete on that level.

- Intensifying competitive pressure — digital challengers and neobanks are eating up your market share by offering next-level customer experiences and employee journeys.

- Evolving technologies — legacy tech doesn’t cut it anymore, and it’s in fact holding many banks back, forcing them to perform constant maintenance, rather than pursue innovation.

To stay competitive, your bank needs to create a digital transformation roadmap and begin modernizing for the future. Believe us when we say that traditional banking is dead, and your bank’s old ways of working won’t last long.

Did you know that

worldwide spending on digital transformation is forecasted to reach almost $4 trillion in 2027, according to IDC?

What’s the difference between digital transformation and modernization in banking?

Although these two concepts are somewhat interchangeable, there’s two key differences that help to distinguish them from each other. For one thing, digital transformation involves so much more than tech, since it covers everything from your bank’s operating model to its culture and beyond. Conversely, banking modernization is largely tech-specific and focuses on overhauling your bank’s legacy systems, point solutions, and operational silos. Secondly, digital transformation is a never-ending process, meaning your bank will need to evolve alongside the industry, whereas modernization can be achieved in three to five years, although you may have to modernize more than once over the lifetime of your bank.

How are banks leveraging digital transformation to enhance the overall customer experience?

Most traditional banks are now aware that every digital transformation is an opportunity to re-architect around the customer — and rightfully so. The inside-out operating models of the past don’t cut it anymore when customers have so many options to choose from. That’s why banks are investing in digital tools, particularly comprehensive mobile and web apps, chatbots, and AI-driven customer service capabilities. Data analytics in particular represent a chance for banks to offer personalized services and offerings, including things like tailored credit cards, mortgages, and other products that are most relevant to the individual customer. And when you combine this with a growing priority on omnichannel strategies, it’s clear that traditional banks are committed to providing a seamless customer experience across both physical and digital channels.

Part 2: the banking flywheel

What is a banking flywheel?

A banking flywheel is a method of digital transformation that allows you to create ongoing, cyclical value for all areas of your business. It’s all about gaining momentum, then using it to power your bank’s operating model and fund new initiatives, eventually creating a self-reinforcing cycle of growth and improvement. Of course, this involves considering how you can deliver customer value and business value, which is demonstrated in the chart below.

![[Blog]-[Featured-image 1]-[What is a banking flywheel]-[EN]](https://cdn.prod.website-files.com/6899ede6858421789bbab873/689c911291ff9f8ac8dfb5a1_image.png)

How can I use my banking flywheel to deliver business value?

If you want to use your flywheel to drive business value, tech debt is your biggest hurdle — but it’s also your gateway to success. First, you should start by moving to a more simplified IT landscape. A common platform architecture in particular can be enormously helpful with this, as it will allow you to gradually decommission your legacy systems. And you’ll soon see the benefits of this approach.

Did you know that

you can quickly reduce your IT costs by 30%, if you prioritize the right things and take an aggressive approach, according to McKinsey.

Once you realize the inevitable cost savings, you’ll be free to reinvest that cash flow in another tech-debt-reduction cycle, and that’s when you’ll be able to improve your agility/speed and even lower your cost to income ratio, as demonstrated in the chart below.

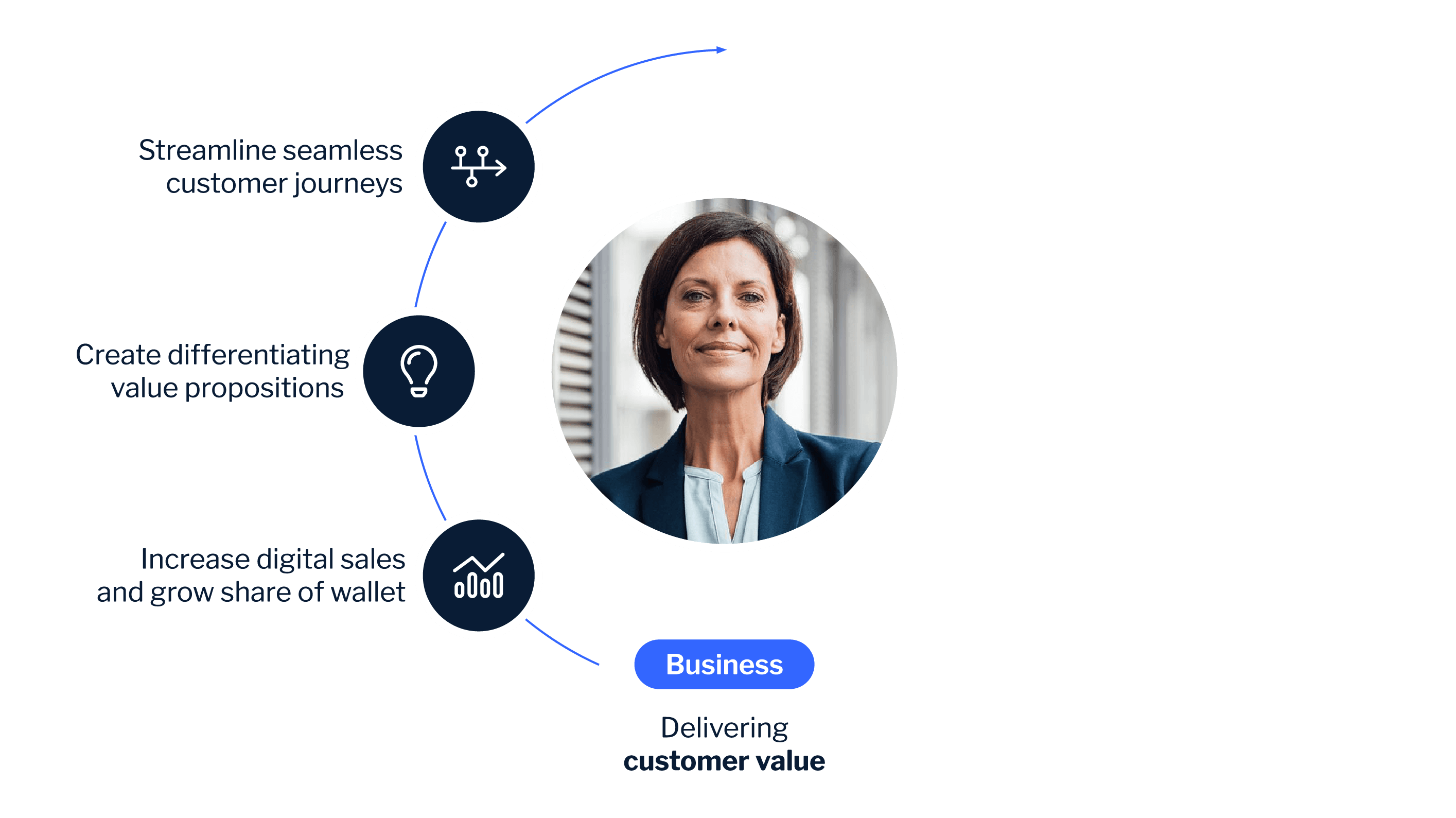

How can I use my banking flywheel to drive customer value?

Using your flywheel to drive customer value begins with streamlining your fragmented customer journeys — the biggest point of friction out there. Rather than investing money towards keeping your legacy systems and tech alive, you should become brutally focused on making these journeys as seamless as possible. If you can pull that off, you’ll have more funds for differentiation, which will, in turn, allow you to increase digital sales and grow your share of wallet. In the process, you’ll eventually create a winning formula that can basically self-finance itself, as you can see here in the chart.

How can I harmonize my bank’s flywheel to enable continuous innovation?

To create shared synergies between the two sides of your banking flywheel, start by using a unified platform model to simplify your existing tech infrastructure, then watch as the cost savings roll in and your agility skyrockets. Now, rather than investing in further tech reduction, you can reallocate funds towards streamlining your customer journeys, which will help you generate both business and customer value. In doing so, you’d dovetail the two areas together, accelerating both in ways that would never be possible in isolation. As you continue using your funds to improve the customer experience, you’d gain new opportunities for cross- and up-sell, as well as growing market share. Then, you can turn around and reinvest in the tech side of your flywheel, and so on, and so on. Check out the chart below for a visual representation of what this might look like.

![[Blog]-[Featured-image 2]-[What is a banking flywheel]-[EN]](https://cdn.prod.website-files.com/6899ede6858421789bbab873/689c9140d2669981b4184cbf_image.png)

Part 3: progressive modernization

What is modernization in banking?

Modernization in banking refers to the ways through which your bank updates and improves its existing systems, infrastructure, and processes, allowing you to enhance operational efficiency, improve existing processes, and reduce costs. And while this does make it more tech-focused than a digital transformation, it’s no less important. After all, with legacy systems in place, it’s all but impossible to compete in a crowded market, let alone deliver real customer value. And to make matters worse, banks are lagging behind compared to other industries when it comes to modernization.

Did you know that

the average age of bank IT applications is among the highest across industries at an estimated 14 years, compared to 4.5 years for retailers, according to McKinsey.

How are banks modernizing their core banking systems?

The days of monolithic, siloed core banking systems are over — and that’s a good thing, both for your bank and its customers. As IT models begin to shift away from in-house, self-built legacy systems, banks are increasingly hollowing out their cores, allowing them to invest in modern, cloud-based systems and platforms that are provided and managed by third-party vendors. Unfortunately, despite many modern advances, this still entails difficulty when dealing with things like integrations, multiple code bases, and point solutions that have stacked up over years. Another key challenge is the necessity to balance innovation with maintaining stable, secure, compliant systems. Many have turned to a unified platform model to solve this issue, which has also proven successful in generating ongoing value, as well as decomposing their bank’s complexity.

What are the top 3 approaches for modernizing my bank?

Like McKinsey, we see three clear paths to banking modernization:

- Big bang replacement — overhauling the user interface, core systems, and integrations all at the same time with a monolithic system update.

- Greenfield approach — reusing elements from your existing infrastructure to quickly create a cloud-native tech stack.

- Progressive modernization — leveraging incremental, iterative improvements to modernize your most important customer journeys and underlying processes.

Our recommendation is progressive modernization, the middle-of-the-pack option that gives you medium speed and cost, but at significantly lower risk. Unlike the other approaches, a progressive modernization is suitable for almost every bank.

What is progressive modernization in banking?

Progressive modernization in banking involves four key steps:

- Assess your needs — evaluating your existing systems, processes and tech while taking care to solicit feedback from customers and employees

- Strategize a way forward — defining clear objectives, isolating burning issues in an agile, cross-functional team, and creating a modernization roadmap that includes a true strategic partner

- Implement your strategy — modernizing on a journey-by-journey basis, prioritizing high-impact, customer-facing areas that will immediately demonstrate value

- Repeat the process — using your newly created digital factory to start over, preferably by adopting open banking standards and an industry-specific integration platform-as-a-service (IPaaS).

Once you’re done, don’t forget to continuously monitor and improve your new tech and systems, assessing them against predefined metrics and KPIs.

What are the three key approaches for performing a progressive banking modernization?

Once you’ve selected a progressive modernization, you’ll need to choose between three key approaches:

- Segment-based — starting at the business segment level, typically on the onboarding or servicing side of things, and replacing existing apps/services

- Journey-based — selecting a single journey to modernize, front-to-back, beginning with the ones that are in need of an overhaul and have a positive ROI or cost impact.

- Headless — rewiring your core systems and adopting a digital banking platform that will power your different channel applications, allowing you to reduce logic duplication across your tech stack.

How you choose will depend on things like your bank’s needs, as well as its size and resources, so be careful to critically consider these issues before you begin on your journey.

Taking the first step

Now that you better understand the complex topic of modernization in banking, there’s plenty of next-best actions you can take. Our weekly Banking Reinvented podcast is a great way to stay up-to-date with modernization trends and developments as you hear from our leadership and chief executives from across the industry. If you'd prefer to dive right in, you can check out our step-by-step guide to progressive banking modernization, written by Backbase Founder/CEO, Jouk Pleiter. And if you’re eager to actually get started, feel free to reach out to our experts. We’re standing by to help, and our top priority is the success of your bank’s modernization journey.